You open your mailbox and there it is: a letter from your insurance company. The words "policy change" jump out at you, and your stomach drops a little. After reading through the insurance jargon, you realize your roof coverage has switched from RCV to ACV.

Wait, what?

If you're scratching your head right now, you're not alone. Thousands of Illinois homeowners are receiving similar notices, and most have no idea what it actually means until they file a claim and get hit with a much smaller check than expected.

Let's break down what's happening with roof insurance in Illinois, why it matters to your wallet, and what you can do about it.

The Big Switch: What's Happening in Illinois

Insurance companies across Illinois have been quietly switching older roofs from Replacement Cost Value (RCV) coverage to Actual Cash Value (ACV) coverage. This isn't just affecting a few unlucky homeowners: it's becoming the new standard for roofs that are typically 15-20 years old or older.

You might be wondering: "Did I do something wrong? Is my insurance company trying to screw me over?"

Not exactly. But understanding the difference between these two types of coverage is crucial, because it can mean thousands of dollars out of your pocket when you need a roof repair or replacement.

ACV vs. RCV: What's the Actual Difference?

Let's cut through the insurance speak and explain this in plain English.

Replacement Cost Value (RCV) is the good stuff. If a hailstorm damages your roof, your insurance pays what it would cost to replace it with a new roof today: regardless of how old your current roof is. You pay your deductible, and the insurance covers the rest of the replacement cost. Simple.

Actual Cash Value (ACV) is different. With ACV, your insurance company calculates what your roof is "worth" at the time of damage based on its age and condition. They take the replacement cost and subtract depreciation. The result? A much smaller payout.

Here's a real-world example that'll make this crystal clear:

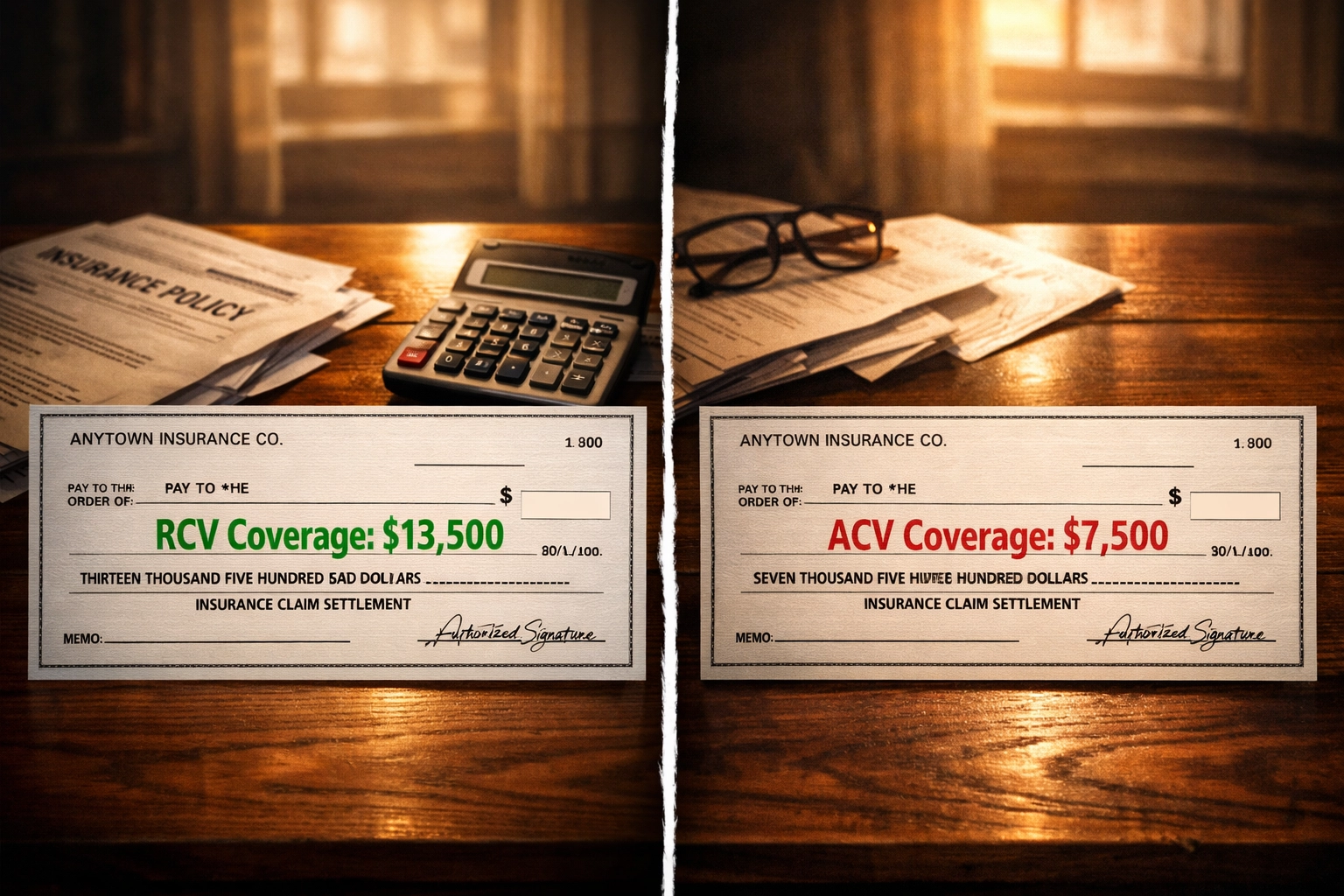

Let's say you have a 12-year-old roof that gets destroyed in a severe Illinois storm. A new roof would cost $15,000 to replace.

- With RCV coverage: You pay your $1,500 deductible. Insurance pays $13,500. You're good to go.

- With ACV coverage: The insurance adjuster determines your 12-year-old roof has depreciated by $6,000. You pay your $1,500 deductible, insurance pays $7,500, and you're stuck covering the remaining $6,000 out of pocket.

That's a $6,000 difference just because of depreciation.

Why Are Insurance Companies Making This Switch?

You might be thinking, "This seems unfair. Why are they doing this?"

The insurance industry will tell you it's about risk management. Older roofs are more likely to have damage, more likely to fail during storms, and more expensive to insure. From their perspective, they're paying for a "used" roof, not a brand new one.

But here's what it really means for you: insurance companies are shifting more financial responsibility onto homeowners with older roofs.

And in Illinois, where we deal with everything from brutal winter storms to summer hail and high winds, your roof takes a serious beating. This makes the ACV switch particularly painful for Illinois homeowners.

The Real Impact on Your Wallet

Let's talk numbers, because this is where it gets personal.

If you're paying for ACV coverage, you're probably saving about 20-25% on your insurance premiums compared to RCV coverage. That sounds great until you actually need to file a claim.

Here's a breakdown of what you could be facing:

Scenario 1: Minor Storm Damage

- Repair cost: $3,500

- Depreciation on 10-year-old roof: $1,200

- Your deductible: $1,500

- Insurance pays: $800

- You pay: $2,700 out of pocket

Scenario 2: Full Roof Replacement

- Replacement cost: $18,000

- Depreciation on 15-year-old roof: $8,000

- Your deductible: $1,500

- Insurance pays: $8,500

- You pay: $9,500 out of pocket

In the second scenario, you're basically paying for half of a new roof yourself. And if your roof is even older: say 18-20 years: the depreciation could be so high that your insurance payout barely covers a quarter of the replacement cost.

For roofs that are extremely old or poorly maintained, some homeowners find their ACV payouts are minimal or even zero. That's right: you could be paying insurance premiums for years and still get almost nothing when you actually need help.

What This Means for Illinois Homeowners Right Now

Here's the bottom line: if your roof is 10+ years old and you have ACV coverage, you need to be financially prepared for a significant out-of-pocket expense if damage occurs.

This is especially important in Illinois because:

Our weather is unpredictable and harsh. We get heavy snow loads in winter, severe thunderstorms and hail in spring and summer, and wind damage year-round.

Roof lifespan matters more than ever. If your roof is approaching 15-20 years old, you're in that danger zone where depreciation really starts to add up.

The longer you wait, the worse it gets. Every year your roof ages, the depreciation increases, meaning your potential out-of-pocket costs go up.

Why Regular Roof Inspections Are Now Critical

Here's where a lot of homeowners are getting caught off guard: minor roof damage that goes unnoticed can turn into major problems that cost you thousands.

When you have ACV coverage, you can't afford to let small issues slide. That missing shingle, that small leak, that worn flashing around your chimney: these aren't "deal with it later" problems anymore. They're ticking time bombs for your wallet.

This is why regular roof inspections from a professional team like TCI Roofing are more important than ever. We can:

- Catch problems early before they turn into insurance claims with huge out-of-pocket costs

- Document your roof's condition so you have proof of proper maintenance

- Provide maintenance that extends your roof's lifespan and reduces depreciation

- Give you an honest assessment of whether repair or replacement makes more financial sense

Think of it this way: spending a few hundred dollars on professional inspections and minor repairs now could save you thousands later when you're not stuck covering massive depreciation costs.

What You Can Do About It

If you've received that dreaded letter about your coverage switching to ACV, here are your options:

Option 1: Ask About RCV Coverage

Some insurance companies will still offer RCV coverage for older roofs, but you'll pay higher premiums. Do the math: if the premium difference is less than the potential depreciation, it might be worth it.

Option 2: Invest in Roof Maintenance

Regular maintenance and minor repairs can extend your roof's lifespan and potentially keep its "value" higher in the eyes of insurance adjusters. Plus, a well-maintained roof is less likely to fail in the first place.

Option 3: Consider Strategic Replacement

If your roof is 15+ years old and you have ACV coverage, it might make financial sense to replace it proactively before a storm forces your hand. A new roof gives you:

- Better protection

- Potentially better insurance coverage options

- Peace of mind

- A roof that won't cost you thousands in depreciation if damage occurs

Option 4: Get Professional Documentation

Have your roof professionally inspected now. Get documentation of its current condition, remaining lifespan, and any maintenance performed. This information can be valuable when dealing with insurance adjusters after a claim.

The Bottom Line

The insurance industry's shift to ACV coverage for older roofs isn't going away. If anything, more companies are likely to follow this trend. As an Illinois homeowner, understanding what this means for your wallet is the first step in protecting yourself.

The key takeaway? Don't ignore your roof. What used to be "just an insurance problem" is now potentially a major expense that could blindside you during an already stressful time.

At TCI Roofing, we've seen too many homeowners get caught off guard by ACV coverage. They thought they were fully covered, only to discover they're on the hook for thousands of dollars after storm damage.

The good news? With proper maintenance, regular inspections, and honest guidance from roofing professionals who actually care about protecting your investment, you can navigate this new insurance reality without getting burned.

Want to know where your roof stands? We offer comprehensive roof inspections for Illinois homeowners that give you a clear picture of your roof's condition, estimated remaining lifespan, and honest recommendations: no pressure, no gimmicks. Just straight talk about what your roof needs and what it'll cost.

Because at the end of the day, your roof is more than just shingles and nails. It's protection for your family and your biggest investment. And that's worth taking care of properly.

{kind=link}

{kind=link}

1 comment